India Ratings Affirms AYM Syntex At ‘IND A’/Stable; Off RWN

India Ratings and Research (Ind-Ra) has affirmed AYM Syntex Limited’s (AYM) Long-Term Issuer Rating at ‘IND A’ with a Stable Outlook, while resolving the Rating Watch Negative (RWN).

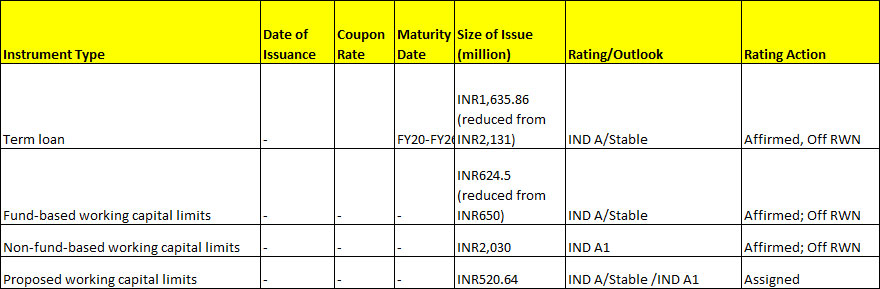

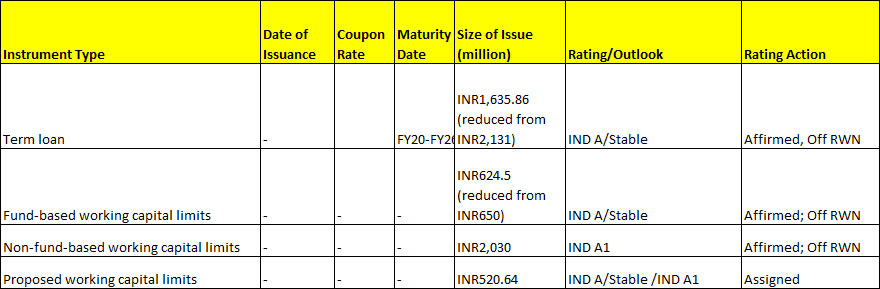

The instrument-wise rating actions

The RWN resolution reflects an improvement in AYM’s short-term liquidity position, which led to a recovery in demand over 2HFY21, resulting in stronger-than-expected operational cash flows in FY21; the sanction of additional working capital limits and the availment of low-cost debt facilities with elongated maturity profile, easing the repayment pressure. The higher operating cash flows in FY21 were a result of i) higher share of value-added products and exports ii) cost-cutting initiatives, iii) higher spreads on key products and iv) inventory gains.

Recovery in operational performance

AYM logged revenue of Rs 9,474 million in FY21 (FY20: Rs 10,280 million) and EBITDA of Rs 913.6 million (Rs 943 million). The company EBITDA’s turned negative to Rs 59.8 million in 1QFY21 (4QFY21: Rs 419 million; 3QFY21: Rs 349 million; 2QFY21: Rs 206 million; FY20: Rs 943 million; FY19: Rs 716 million). The improvement in quarterly performance over FY21 can be attributed to demand recovery, both in the domestic and export market, and an increased share of value-added products including bulk continuous filament (BCF) yarn and heat set yarn, within the overall product mix, and higher crude oil prices resulting in inventory gains. Ind-Ra believes export demand is likely to be strong, although with challenges on the availability of containers and increased shipping and freight costs.

Plant utilisations have witnessed quarterly improvement over FY21, within each business segment, led by an increase in the capacity utilisation and efficiency levels. Ind-Ra expects the company’s FY22 sales volumes to grow around 15% yoy, due to the low base effect of FY21 (due to COVID-19 impacting 1QFY21 volumes) and an improved throughput.

AYM’s sales book is largely order backed and the management has articulated that it typically maintains a two-to-three month order book in strategic segments, thereby providing near-term revenue visibility.

The RWN resolution reflects an improvement in AYM’s short-term liquidity position, which led to a recovery in demand over 2HFY21, resulting in stronger-than-expected operational cash flows in FY21; the sanction of additional working capital limits and the availment of low-cost debt facilities with elongated maturity profile, easing the repayment pressure. The higher operating cash flows in FY21 were a result of i) higher share of value-added products and exports ii) cost-cutting initiatives, iii) higher spreads on key products and iv) inventory gains.

Recovery in operational performance

AYM logged revenue of Rs 9,474 million in FY21 (FY20: Rs 10,280 million) and EBITDA of Rs 913.6 million (Rs 943 million). The company EBITDA’s turned negative to Rs 59.8 million in 1QFY21 (4QFY21: Rs 419 million; 3QFY21: Rs 349 million; 2QFY21: Rs 206 million; FY20: Rs 943 million; FY19: Rs 716 million). The improvement in quarterly performance over FY21 can be attributed to demand recovery, both in the domestic and export market, and an increased share of value-added products including bulk continuous filament (BCF) yarn and heat set yarn, within the overall product mix, and higher crude oil prices resulting in inventory gains. Ind-Ra believes export demand is likely to be strong, although with challenges on the availability of containers and increased shipping and freight costs.

Plant utilisations have witnessed quarterly improvement over FY21, within each business segment, led by an increase in the capacity utilisation and efficiency levels. Ind-Ra expects the company’s FY22 sales volumes to grow around 15% yoy, due to the low base effect of FY21 (due to COVID-19 impacting 1QFY21 volumes) and an improved throughput.

AYM’s sales book is largely order backed and the management has articulated that it typically maintains a two-to-three month order book in strategic segments, thereby providing near-term revenue visibility.

Textile Excellence

Subscribe To Textile Excellence Print Edition

If you wish to Subscribe to Textile Excellence Print Edition, kindly fill in the below form and we shall get back to you with details.

Newsletter

Subscribe To Textile Excellence Mailing List

- December 09, 2022

'There Is Very High Acceptance For India

- December 09, 2022

'Advanced Machines & Service, Customer C

- October 09, 2023

First-time In The World: Rieter’s Auto

- October 31, 2023

Denge & Dyesol India: Leading The Way In

- June 01, 2020

Karl Mayer Enables Automated Production

- June 05, 2023

Ultimax - All New Revolutionary Rapier W

- June 09, 2025