Global Apparel Trade Under Pressure Amid Weak Demand Signals

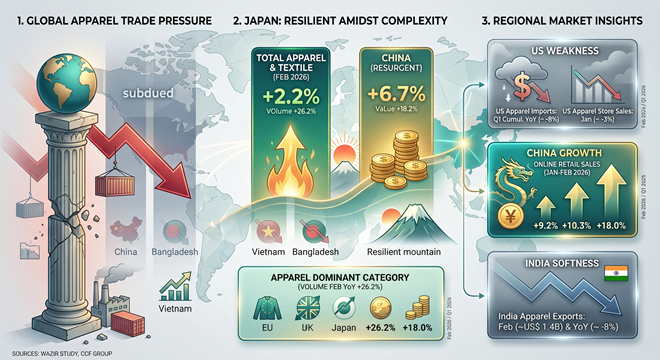

Global apparel trade continues to face near-term pressure as demand remains uneven across key markets. While the EU and UK are showing relative stability, the US and Japan continue to reflect subdued import demand, resulting in an overall ~8% year-on-year decline in cumulative imports.

The supplier landscape is also shifting. Traditional leaders such as China and Bangladesh are under pressure, while Vietnam is steadily gaining share, indicating a gradual but clear rebalancing of global sourcing.

India’s apparel exports stood at ~US$ 1.4 billion in February 2026, down around 8% year-on-year, pointing to continued softness in export momentum.

On the demand side, the US remains weak, with apparel store sales at ~US$ 14.2 billion in January, down ~3%, alongside a sharper decline in the home category. Retail and e-commerce trends remain mixed globally, underscoring uncertain consumption patterns and cautious buying behaviour. These are some of the findings from the latest textile and apparel exports study by Wazir.

Japan imports show resilience despite short-term dip

However, according to China’s CCF Group, Japan’s textile and apparel import trends present a more nuanced picture within an otherwise uncertain global environment. While imports declined month-on-month in February 2026, largely due to seasonal factors, the broader trajectory remains positive, supported by a low base and relatively resilient end demand.

The Japanese economy continues to recover at a moderate pace, though underlying conditions remain fragile. Inflationary pressures have eased, with core CPI falling below the Bank of Japan’s 2% target.

However, external headwinds persist. Export growth is slowing amid volatile global energy prices and weakening international demand, while the yen remains under depreciation pressure. Domestic consumption also faces constraints due to high price levels and sluggish real wage growth. Although tourism continues to support economic activity, a decline in visitors from mainland China has added another layer of uncertainty.

Against this backdrop, Japan’s textile and apparel imports declined in February, with total volumes reaching 203,000 tonnes, down 5.8% month-on-month. This drop was largely attributed to production disruptions in supplier countries during the Lunar New Year period, along with advance stocking of spring orders in January. In value terms, imports stood at 408.15 billion yen, down 5.7% from the previous month.

However, the year-on-year comparison tells a different story. Imports rose 18.8% in volume and 23.1% in value, reflecting a strong recovery from last year’s lower base. On a cumulative basis, imports for January–February reached 418,000 tonnes, up 7.1% year-on-year, while total value increased 13.9% to 840.87 billion yen.

A key trend shaping Japan’s sourcing dynamics is the strong resurgence of China. Imports from China have grown significantly, both in volume and value, indicating a clear expansion in market share. In February alone, imports from China reached 111,000 tonnes, up 45.5% year-on-year, while import value rose over 50%. On a cumulative basis, China’s share continued to strengthen, supported by its ability to quickly resume production after the holiday period and efficiently execute orders.

Apparel remains the dominant category within imports. In February, Japan imported 77,000 tonnes of apparel, reflecting a 26.2% year-on-year increase in volume. This suggests that despite macroeconomic pressures, underlying consumer demand for apparel has remained relatively stable.

Notably, a divergence has emerged among key supplier countries. While overall apparel imports declined month-on-month, imports from China actually increased slightly, driven by faster post-holiday recovery and concentrated shipment cycles.

In contrast, suppliers such as Vietnam and Bangladesh experienced declines, highlighting differences in supply chain responsiveness and production timelines.

In the near term, Japan’s import trends are likely to remain influenced by seasonality and macroeconomic uncertainty. However, the resilience seen in year-on-year growth indicates that demand has not weakened structurally. Instead, the market is adjusting to short-term disruptions.

Going forward, factors such as global demand conditions, currency movements, and the ability of supplier countries to maintain consistent delivery cycles will play a critical role. For now, Japan stands out as a market where short-term softness coexists with underlying demand stability, even as global apparel trade navigates a challenging phase.

China’s domestic clothing market continues to grow

From January to February 2026, online retail sales of goods and services in China reached 3,254.58 billion yuan, up 9.2% year-on-year. Among this, online retail sales of physical goods stood at 2,081.2 billion yuan, an increase of 10.3% year-on-year; online retail sales of clothing grew by 18%, online retail sales of food rose by 20.7%, and online retail sales of other goods increased by 4.7%. Online retail sales of services reached 1,173.38 billion yuan, up 7.3% year-on-year.

On the demand side, the US remains weak, with apparel store sales at ~US$ 14.2 billion in January, down ~3%, alongside a sharper decline in the home category. Retail and e-commerce trends remain mixed globally, underscoring uncertain consumption patterns and cautious buying behaviour. These are some of the findings from the latest textile and apparel exports study by Wazir.

Subscribe To Textile Excellence Print Edition

If you wish to Subscribe to Textile Excellence Print Edition, kindly fill in the below form and we shall get back to you with details.

Newsletter

Subscribe To Textile Excellence Mailing List

- December 09, 2022

'There Is Very High Acceptance For India

- December 09, 2022

'Advanced Machines & Service, Customer C

- October 09, 2023

First-time In The World: Rieter’s Auto

- October 31, 2023

Denge & Dyesol India: Leading The Way In

- June 01, 2020

Karl Mayer Enables Automated Production

- June 05, 2023

Ultimax - All New Revolutionary Rapier W

- June 09, 2025