East Africa Emerges As High Return Textile Destination For Indian Players

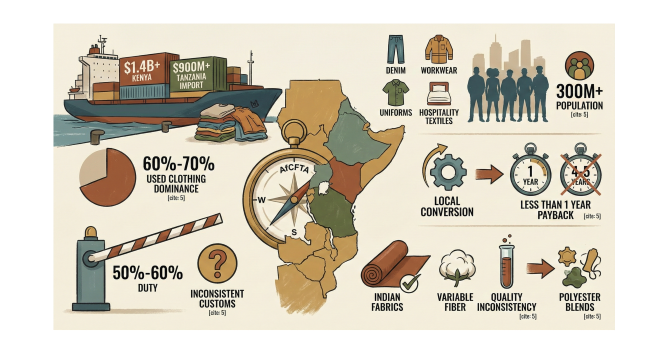

East Africa is gaining attention as a strategic textile destination, supported by rising consumption, urbanisation and regional integration under the African Continental Free Trade Area. The region remains heavily import dependent. Kenya alone imported textiles and apparel worth over US$ 1.4 billion in 2023, while Tanzania’s imports crossed US$ 900 million, reflecting strong reliance on foreign supply.

Industry estimates indicate more than 60% to 70% of apparel consumption in several East African markets still comes from secondhand clothing, leaving a defined but growing space for new fabrics and value driven products.

Import Driven Demand Creates Niche Opportunities

Despite dominance of used clothing, the remaining organised segment is expanding steadily. Demand is strongest in denim, workwear, uniforms and hospitality textiles. Urban youth populations are growing rapidly. The East African Community population has crossed 300 million, offering long-term consumption potential.

Institutional buyers such as schools, factories and hotels continue to rely on imported fabrics due to inconsistent local supply and limited finishing capabilities.

Duty Barriers Persist But Indian Products Remain Competitive

Import duties on finished fabrics often reach 50% to 60% across several African markets. Even at these levels, Indian fabrics remain competitive due to better shade control, consistent quality, and efficient conversion costs.

However, customs practices remain inconsistent in certain markets. Duty assessment may vary depending on classification, local interpretation and clearance procedures, making experienced local handling critical.

Raw Material Gaps Drive Man Made Fibre Growth

East Africa grows cotton but quality inconsistency remains a major challenge. Fibre length variation and contamination issues limit spinning performance.

Polyester viscose and polyester cotton blends are gaining traction across school uniform and workwear segments. These fabrics offer better durability, lower cost and improved wash resistance under harsh climatic and laundering conditions.

Low Investment Conversion Model Offers Faster Payback

Importing finished fabrics attracts heavy duties, but raw material imports face lower tariffs. This creates a strong case for local conversion units such as dyeing, finishing and garmenting.

Industry practitioners report payback periods of less than one year in African conversion operations, compared to four to five years in India for similar investments. East Africa presents a practical growth market rather than a friction-free one. Success depends on shade adaptation, simple conversion strategies, and local operational understanding.

East Africa grows cotton but quality inconsistency remains a major challenge. Fibre length variation and contamination issues limit spinning performance. Polyester viscose and polyester cotton blends are gaining traction across school uniform and workwear segments. These fabrics offer better durability, lower cost and improved wash resistance under harsh climatic and laundering conditions.

Subscribe To Textile Excellence Print Edition

If you wish to Subscribe to Textile Excellence Print Edition, kindly fill in the below form and we shall get back to you with details.

Newsletter

Subscribe To Textile Excellence Mailing List

- December 09, 2022

'There Is Very High Acceptance For India

- December 09, 2022

'Advanced Machines & Service, Customer C

- October 09, 2023

First-time In The World: Rieter’s Auto

- October 31, 2023

Denge & Dyesol India: Leading The Way In

- June 01, 2020

Karl Mayer Enables Automated Production

- June 05, 2023

Ultimax - All New Revolutionary Rapier W

- June 09, 2025