Australia’s Cotton Exports Rise As China And India Drive Demand

Australia’s cotton exports

are set to rise sharply despite an expected dip in production, underscoring how

global demand shifts and stock dynamics are rewriting trade flows in real time.

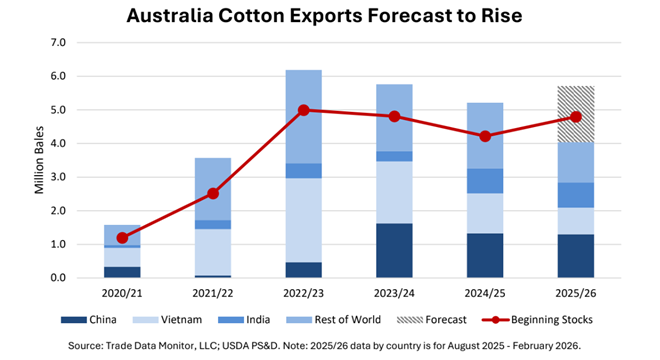

For the 2025/26 marketing year (August 2025–July 2026), exports are forecast to

climb nearly 10% to 5.7 million bales, powered by strong buying from China and

India that more than offsets weaker shipments to Vietnam.

The surprising resilience

is being driven not by a bigger crop, but by timing and inventory. A large

2024/25 harvest has left Australia with elevated beginning stocks, effectively

front-loading supply into the current export cycle. These stocks are now acting

as a buffer, allowing exports to stay strong even before the smaller 2025/26

crop enters the market.

Australia’s export rhythm

also plays a decisive role. As a Southern Hemisphere producer, harvesting

begins in April, with exports typically starting in May. Roughly 30% of the new

crop is shipped in the final quarter of the marketing year, while the rest is

carried into the next cycle. That means exports between May and July will

increasingly reflect tighter supply conditions from the new crop.

On the demand side, the

geography of trade is shifting fast. As of February, China accounts for about

one-third of Australia’s cotton exports, while Vietnam and India each absorb

roughly one-fifth. This balance has changed dramatically over the past few years.

During 2021/22 and 2022/23, political tensions pushed China away from

Australian cotton, redirecting flows toward Vietnam. That pattern has now

reversed as China returns as a dominant buyer.

India has emerged as

another key swing factor. Temporary duty removal between August and December

2025 triggered a surge in imports, with Australian shipments already surpassing

last year’s totals. Together, China and India are now reshaping Australia’s export

map.

However, this concentration

carries risk. Around 70% of Australia’s exports are now tied to just three

markets, leaving it more exposed to geopolitical and policy shocks than Brazil

or the United States, where demand is more diversified.

Globally, cotton

fundamentals remain mixed. Production is expected to rise to 121.9 million

bales, driven by China, India, and Pakistan, while consumption edges up to

119.1 million bales. Trade volumes, however, are slightly lower at 43.7 million

bales due to weaker flows from India and softer import demand in several Asian

markets.

Ending stocks are also

rising to 77 million bales, led by accumulation in China and India—signalling

that even as demand strengthens, supply is staying ahead of it. In this

shifting balance, Australia’s export surge stands out as a story of timing,

trade realignment, and market concentration risk playing out simultaneously.

Globally, cotton fundamentals remain mixed. Production is expected to rise to 121.9 million bales, driven by China, India, and Pakistan, while consumption edges up to 119.1 million bales. Trade volumes, however, are slightly lower at 43.7 million bales due to weaker flows from India and softer import demand in several Asian markets.

Subscribe To Textile Excellence Print Edition

If you wish to Subscribe to Textile Excellence Print Edition, kindly fill in the below form and we shall get back to you with details.

Newsletter

Subscribe To Textile Excellence Mailing List

- December 09, 2022

'There Is Very High Acceptance For India

- December 09, 2022

'Advanced Machines & Service, Customer C

- October 09, 2023

First-time In The World: Rieter’s Auto

- July 28, 2026

Arvind Eyes Leadership In India's Premiu

- June 01, 2020

Karl Mayer Enables Automated Production

- June 05, 2023

Ultimax - All New Revolutionary Rapier W

- June 09, 2025

DyStar Becomes A Wholly Owned Subsidiary

- July 28, 2026